.svg)

Finance’s next chapter: The operating system layer

Shopify began as a simple tool for building online stores. Fast forward to today, and it is widely viewed as a unified operating system for commerce. It connects storefronts, point-of-sale systems, payments, inventory, customer data, and analytics into a single platform, giving merchants one system of truth across every channel.

A similar evolution can be seen in communications. Twilio transformed what was once a collection of disparate APIs for SMS, voice, and email into a programmable communications layer that developers build on. Instead of stitching together multiple vendors, teams rely on Twilio as a unified backbone, enabling faster feature delivery and more consistent customer engagement.

The same pattern played out in CRM. By unifying sales funnels, customer service, marketing automation, and analytics into one extensible platform, Salesforce turned what was once a fragmented set of tools into a coherent system that teams can extend and customize at scale.

Across industries, the transformation follows a consistent arc: a shift from disconnected tools to a single foundational layer that manages complexity, data, and orchestration.

What about finance?

Unlike commerce and communications, finance has not yet universally adopted a unifying infrastructure layer. Most financial institutions still operate collections of siloed systems, held together by fragile integrations and, in many cases, manual processes.

Yet the pressure for change is growing.

Research shows that over half of financial institutions report missing business opportunities due to limitations in their current technology stacks, largely driven by outdated and fragmented infrastructure. What we are seeing is not a lack of ambition or innovation, but a structural constraint.

This frustration is a signal of an underlying transition. Finance is on the cusp of its own operating system era.

Why this shift is happening

The modern financial stack was rarely designed end to end. Instead, it was accumulated over time.

Legacy cores, bespoke internal systems, and dozens of external vendors may give the appearance of modernity. Underneath, however, they behave like independent machines stitched together. In the Gulf region, for example, research suggests that more than 87 percent of banks rely heavily on external platforms, yet legacy systems remain central to operations, increasing complexity rather than reducing it. In critical functions such as lending, more than 60 percent of institutions still operate entirely on legacy infrastructure, even as modern tools are layered on top.

These realities help explain why innovation feels slow, why product launches take longer than expected, and why compliance and risk processes often become bottlenecks instead of enablers. Finance is beginning to recognize that incremental tooling is no longer enough. Something more foundational is required.

So what is a financial operating system?

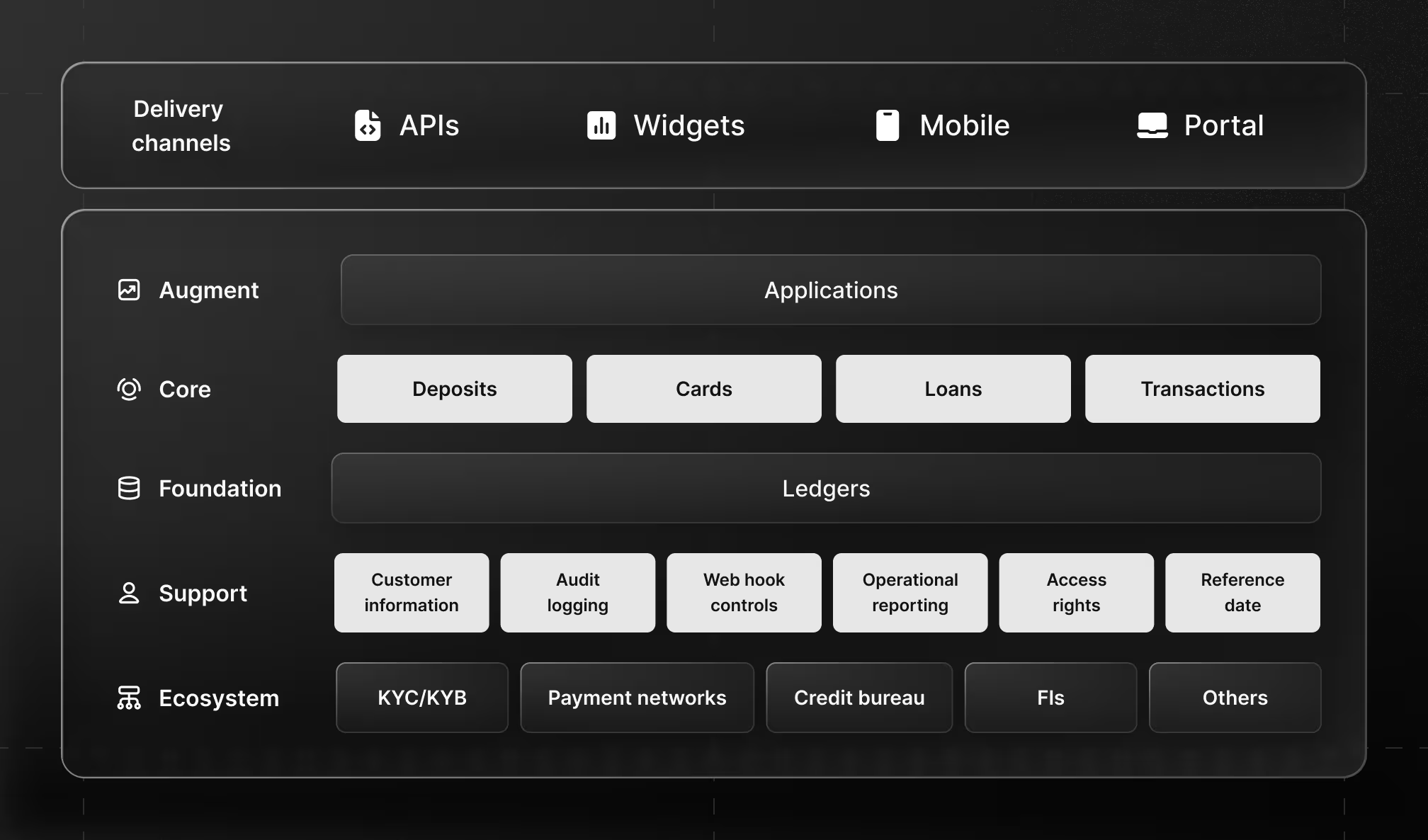

Borrowing from other industries, a financial operating system is a modular and unified infrastructure layer that sits beneath applications and serves as the shared foundation for products, data, and workflows.

An operating system does not force a monolith. Instead, it provides reusable building blocks such as identity and KYC services, ledger and transaction services, risk and compliance engines, payments orchestration, loan management, card lifecycle management, and deposits modules.

Each component can operate independently, while integrating seamlessly with others. This modular approach mirrors how Shopify unified checkout, payments, logistics, and analytics into an extensible commerce layer, and how Twilio unified voice, SMS, email, and identity into a single programmable platform.

A true operating system also enforces shared foundations: a single real-time data model, standardized rules for compliance and risk, and orchestration across products and channels. For end users, customers, partners, and internal teams, this translates into more consistent experiences, faster decisioning, and fewer operational errors. In practice, this can mean real-time compliance embedded into every flow, faster product launches using pre-built services, and unified customer profiles across lending, deposits, and payments.

What financial institutions are demanding

Research shows that institutions consistently cite the same challenges with fragmentation: complex vendor integrations, slow product launch cycles, high operating costs, and difficulty modernizing legacy cores. These pressures are pushing leaders to rethink how their infrastructure is structured.

Across the Gulf, more than two-thirds of decision makers believe a single unified platform would deliver more value than maintaining multiple disconnected solutions. This marks a clear shift in purchasing logic, from best-of-breed silos toward integrated foundations.

In other words, institutions are no longer just looking for better tools, rather they are looking for a system.

Choosing a financial operating system

This shift is also reflected in modernization timelines. Recent studies suggest that a significant majority of financial institutions are planning technology upgrades within the next 12 months, with many pointing to 2026 as the year when foundational transformation accelerates.

Choosing the right operating system layer requires a different lens than traditional vendor selection. Institutions must consider technical architecture, total cost of ownership, team readiness, and how deeply compliance and risk are embedded into the platform. Systems built around modular APIs, real-time data models, and native orchestration are better positioned to replace brittle point-to-point integrations and scale over time.

An operating system is not just a technology decision, rather it is a long-term architectural one.

The impact of an operating system layer

When commerce unified around platforms like Shopify, businesses saw lower total cost of ownership, unified data models, faster omnichannel growth, and fewer integration challenges.

When communications unified around programmable layers like Twilio, teams moved from months-long integrations to days-long experimentation, because the underlying infrastructure handled complexity.

A financial operating system promises similar impact: faster product launches through modular components, lower operational risk through unified compliance and risk logic, cleaner data with real-time decisioning across functions, and greater agility in fast-evolving markets and regulatory environments.

It is clear that finance’s next chapter will be written on a unified operating system layer that turns complexity into composability and enables the next generation of financial innovation.