.svg)

The rise of multi-currency banking

There was a time when businesses expanded internationally in phases. Open a local entity. Open a local bank account. Issue local cards. Manage currency risk separately. That model assumed geography defined commerce.

Today, it no longer does. Digital businesses launch globally from day one. Talent works remotely across jurisdictions. Consumers buy from platforms thousands of kilometers away without thinking about it. Yet much of financial infrastructure still assumes a single base currency. Multi-currency wallets and cards are part of the correction. They reframe currency as a configurable layer within a unified system.

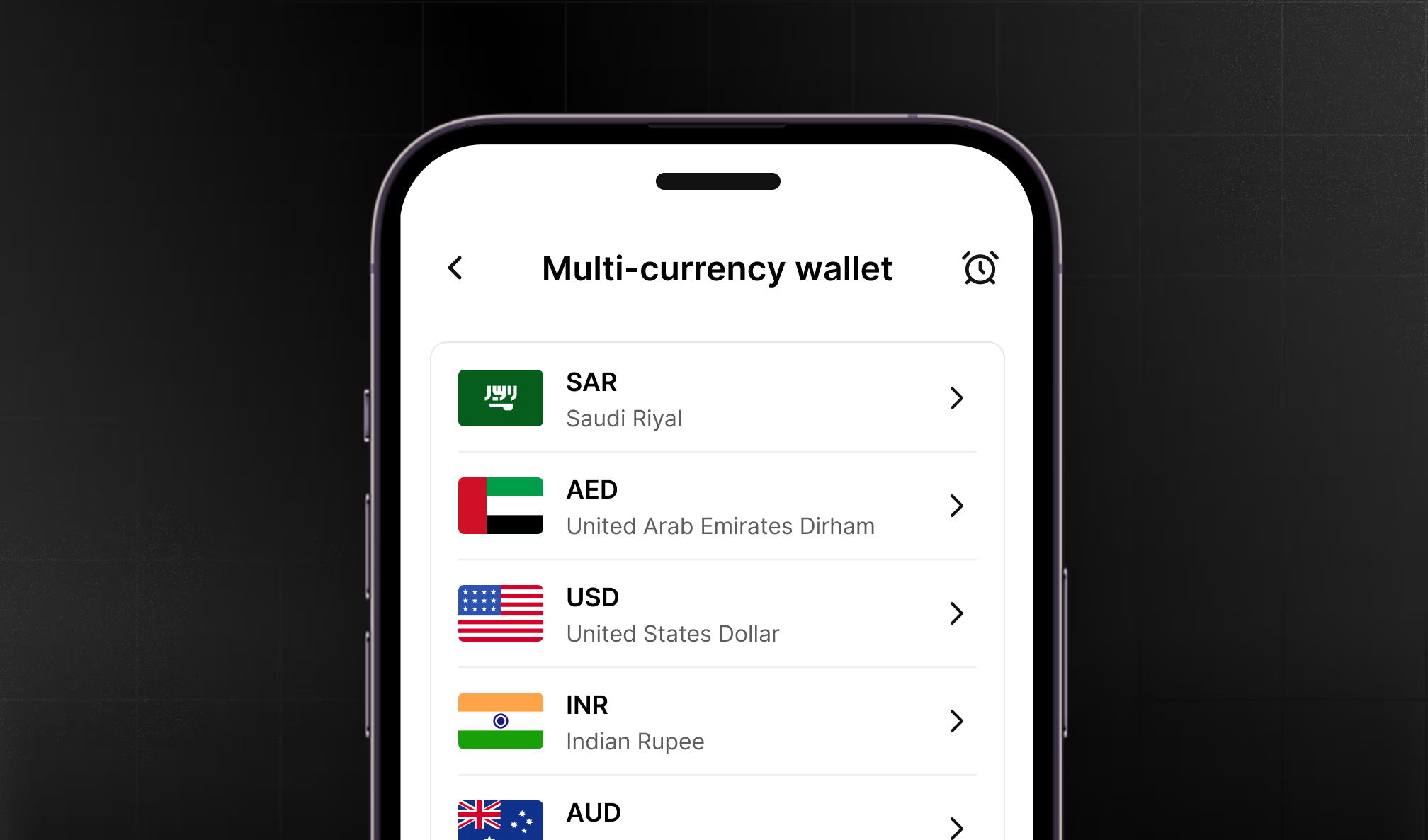

What is a multi-currency wallet?

A multi-currency wallet is a financial account that allows users to hold, manage, send, receive, and convert multiple currencies within a single system. Instead of maintaining separate bank accounts in different jurisdictions, users can hold balances in multiple currencies, receive funds in those currencies, convert between them, and spend directly from selected balances. For individuals, this reduces friction when earning, saving, or spending internationally.

For businesses, it simplifies cross-border operations such as paying global suppliers, receiving payments from international customers, managing FX exposure, and consolidating treasury across markets. At its core, the multi-currency wallet separates currency management from traditional geographic banking constraints.

What is a multi-currency card?

A multi-currency card is typically linked to a multi-currency wallet. It allows users to spend directly from specific currency balances. It can be issued as a prepaid card, debit card, virtual card and in some cases, a credit product layered on top. When a transaction occurs in a supported currency, the card draws from the corresponding balance. If no balance exists in that currency, a real-time FX conversion is triggered. The result is a seamless spending experience across borders using a single card. Beyond just being a travel convenience product, it is a programmable financial surface layered onto wallet infrastructure.

Why they are gaining traction

1. Cross-border commerce is default, not exceptional

Digital businesses operate globally from inception. Marketplaces, SaaS platforms, creator economies, and fintech products serve multi-jurisdiction users. Supporting local currency experiences improves conversion rates, user trust, and pricing transparency. Multi-currency infrastructure enables this at scale.

2. FX transparency and cost control

Traditional banking models often apply opaque foreign exchange spreads and conversion fees at the moment of transaction. Multi-currency wallets allow users to convert proactively, hold balances in anticipation of spend, and optimize timing of FX. This shifts control from the institution to the user or business.

3. Operational simplification for businesses

Without multi-currency infrastructure, businesses often rely on multiple bank accounts across jurisdictions, manual reconciliation processes, external FX brokers, and fragmented treasury systems. A unified wallet consolidates currency balances into a single operational layer, improving visibility and liquidity management.

4. Embedded finance and platform models

Modern platforms increasingly embed financial services directly into their ecosystems. Marketplaces, payroll providers, and vertical SaaS platforms use multi-currency wallets to onboard global users, enable cross-border payouts, issue cards tied to wallet balances, and monetize through FX and interchange. In this context, multi-currency capability becomes a product primitive, not an add-on feature.

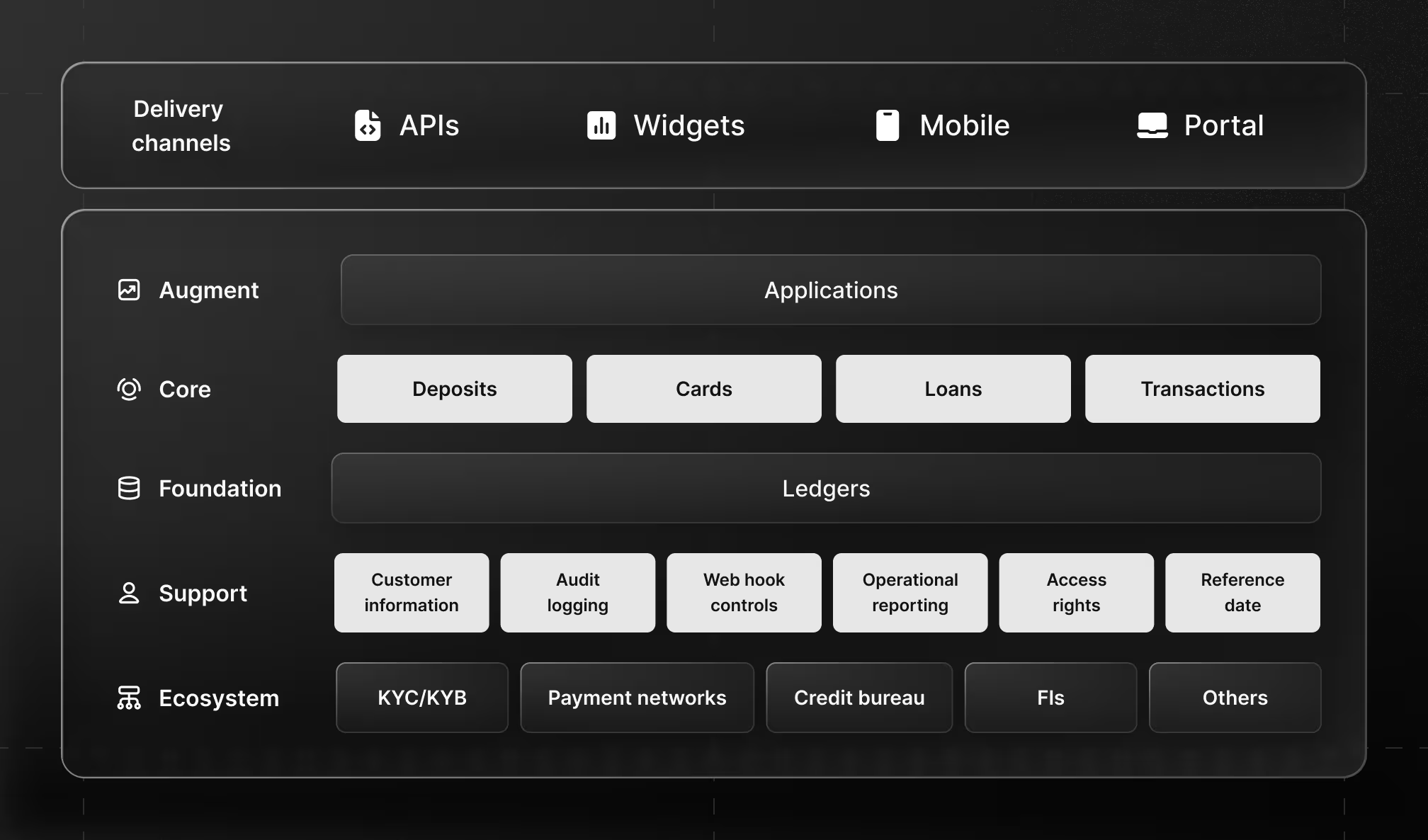

How multi-currency wallets work

At a structural level, three core components operate together.

1. Currency accounts

Behind the wallet interface sit ledgered sub-accounts for each supported currency. Each balance is tracked independently. When funds are received in USD, they settle into the USD ledger. The same applies to EUR, GBP, or any other supported currency. This structure allows true currency segregation rather than continuous conversion into a base currency.

2. Foreign exchange engine

When a user converts between currencies, the wallet, quotes a rate, applies a spread or fee, executes conversion, and updates respective ledger balances. In advanced systems, FX may be real-time, batch processed, hedged, and integrated with liquidity providers. For platforms, this layer often represents a revenue opportunity.

3. Payment rails and settlement

Wallets connect to payment networks and banking rails to receive local transfers, send cross-border payments, support card transactions, and settle merchant payments. This infrastructure typically integrates local clearing systems, card schemes, and correspondent banking networks. The wallet experience abstracts this complexity from the end user.

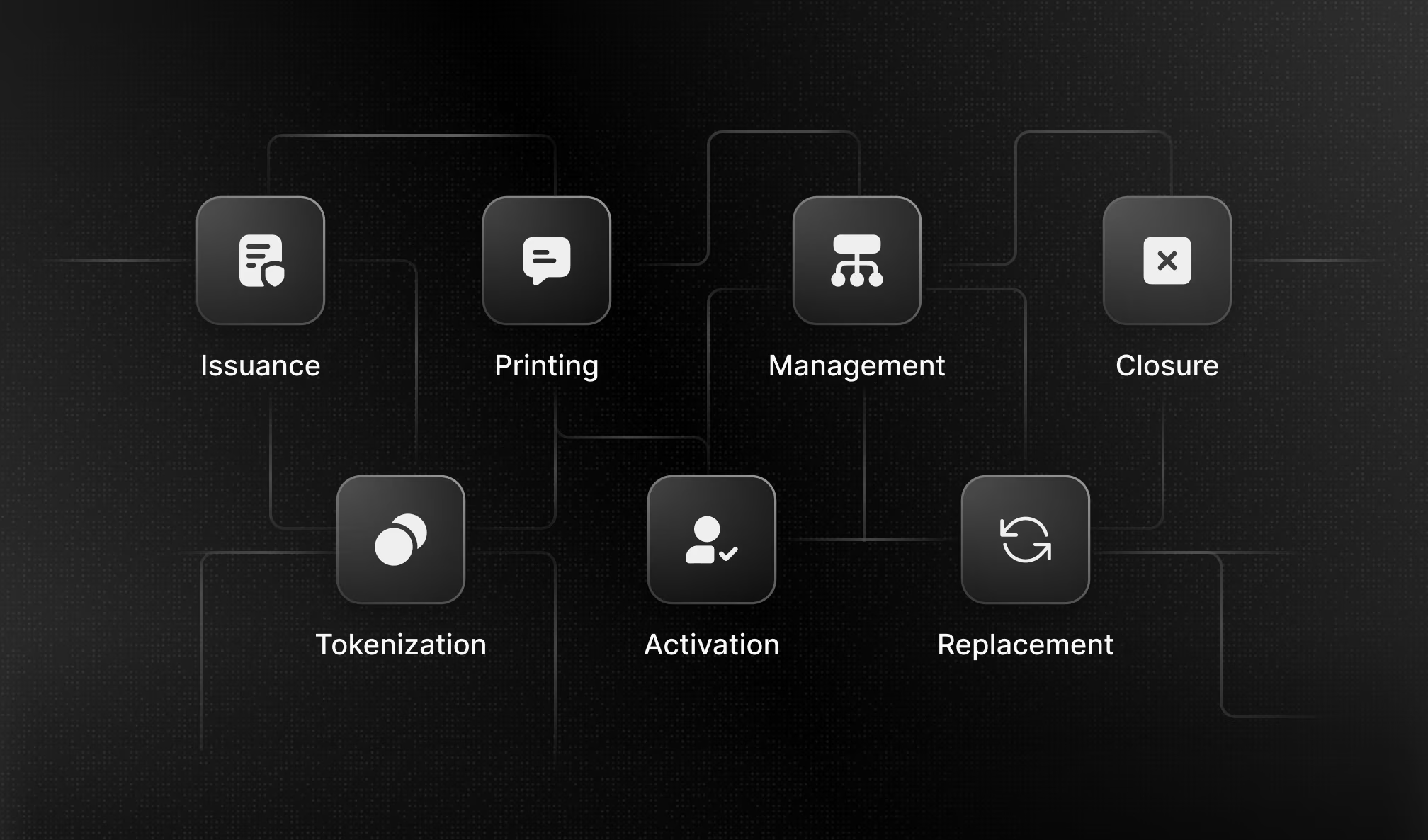

How multi-currency cards work

A multi-currency card sits on top of wallet balances. When a transaction is initiated:

- The merchant sends an authorization request in the local currency.

- The issuer checks if a matching currency balance exists.

- If available, funds are reserved from that balance.

- If not, FX conversion is triggered from another currency balance.

- Settlement occurs through the card network.

From the user perspective, this process is invisible. From an infrastructure perspective, it requires coordination between wallet ledger, FX engine, issuing processor, card network, and settlement bank. This orchestration layer is what enables a single card to behave locally in multiple markets.

The broader shift

Multi-currency cards and wallets reflect a broader transition in financial architecture. From country-bound accounts to programmable, API-driven, globally connected financial systems. As financial services move toward unified infrastructure layers, the ability to manage multiple currencies natively becomes foundational.

In a world where businesses scale globally from inception and individuals operate across borders by default, currency flexibility is becoming standard.