.svg)

From BNPL to RNPL to SNBL: How ‘pay later’ grew up

Consider an individual living an ordinary life in 2026.

Her rent lands on the first. She splits it across two paydays using a platform that pays the landlord upfront. Her groceries go on a card that lets her settle at the end of the month. Her phone is financed over 24 months, bundled into her service plan. And she just booked flights for a holiday which she’s paying for through a BNPL facility.

She may not have thought much about it. But each of these behaviors signals a structural shift in how people relate to money; the timing of payment and the timing of consumption no longer need to match.

The idea is old. What changed is everything else.

The concept of paying later is not new. It is, in fact, embarrassingly old.

By the early 20th century, American factories were churning out washing machines, refrigerators, and radios, and most of them could be bought on installment from the vendor. Layaway as a formal scheme became widespread through the 1930s Depression era, when retailers would hold merchandise while customers paid in stages. Ford's own "Weekly Payment Plan" where buyers deposited small amounts until they had enough to take delivery was eventually crushed by General Motors, who offered the opposite: take the car home today and pay over a year. Americans chose the car now. They have always chosen the thing now.

The credit card followed the same logic at scale. Diners Club launched in 1950 on cardboard. Bank of America mailed two million cards to California customers in 1958, financing purchases and charging interest on unpaid balances. By the end of the Korean War, revolving credit had become a central feature of American commerce. In 1929, one third of all retail sales were already financed.

The desire to decouple possession from payment may look like it is a product of the smartphone era. But it is in fact a feature of human nature that merchants have been monetizing for centuries.

What changed, starting in the early 2010s, is three things: the smartphone put credit decisions in everyone's pocket; APIs made it possible to embed those decisions invisibly into any checkout flow; and real-time data made underwriting fast enough to be frictionless.

The expansion, category by category

Pay-later logic is moving into almost every category of meaningful consumer expenditure, and each expansion unlocks a consumer segment that the original product was never designed to reach.

BNPL remains the most familiar form. The consumer it serves is broadly known: younger, underbanked or credit-averse, shopping online, drawn by the zero-interest split-payment at checkout. The product fits neatly onto the existing retail infrastructure; a widget at checkout, a soft credit decision, four installments.

RNPL moves into entirely different territory. Rent is the single largest monthly expense for most households, and it falls in a lump sum on a fixed date regardless of when paychecks arrive. The tension this creates for gig workers, commission-earners, and anyone on a biweekly pay cycle is structural. In Dubai, Keyper launched an RNPL marketplace that pays landlords the full annual rent upfront while tenants repay monthly.

SNBL inverts the model entirely. Instead of extending credit to the consumer, the merchant holds the consumer's progressive deposits until the purchase amount is reached. No credit risk. No interest. No delinquency. The consumer commits to a future purchase; the merchant receives an interest-free line of capital. It is particularly well-suited to high-consideration purchases, travel, and luxury goods; categories where the consumer wants to plan, not borrow.

Education financing has become one of BNPL's fastest-growing verticals in emerging markets. Traditional education loans require credit histories, collateral, and approval cycles that exclude exactly the families who most need access to learning. Providers like ZestMoney have partnered with universities and vocational centres to offer installment plans for tuition.

Healthcare presents both the clearest need and the most complex terrain. Platforms like PayZen offer patients personalised, interest-free payment plans for healthcare expenses, in partnership with providers.

Travel may be the most intuitive extension of all. MakeMyTrip now lets customers pay 10–40% upfront on international flights and settle the rest within 45 days.

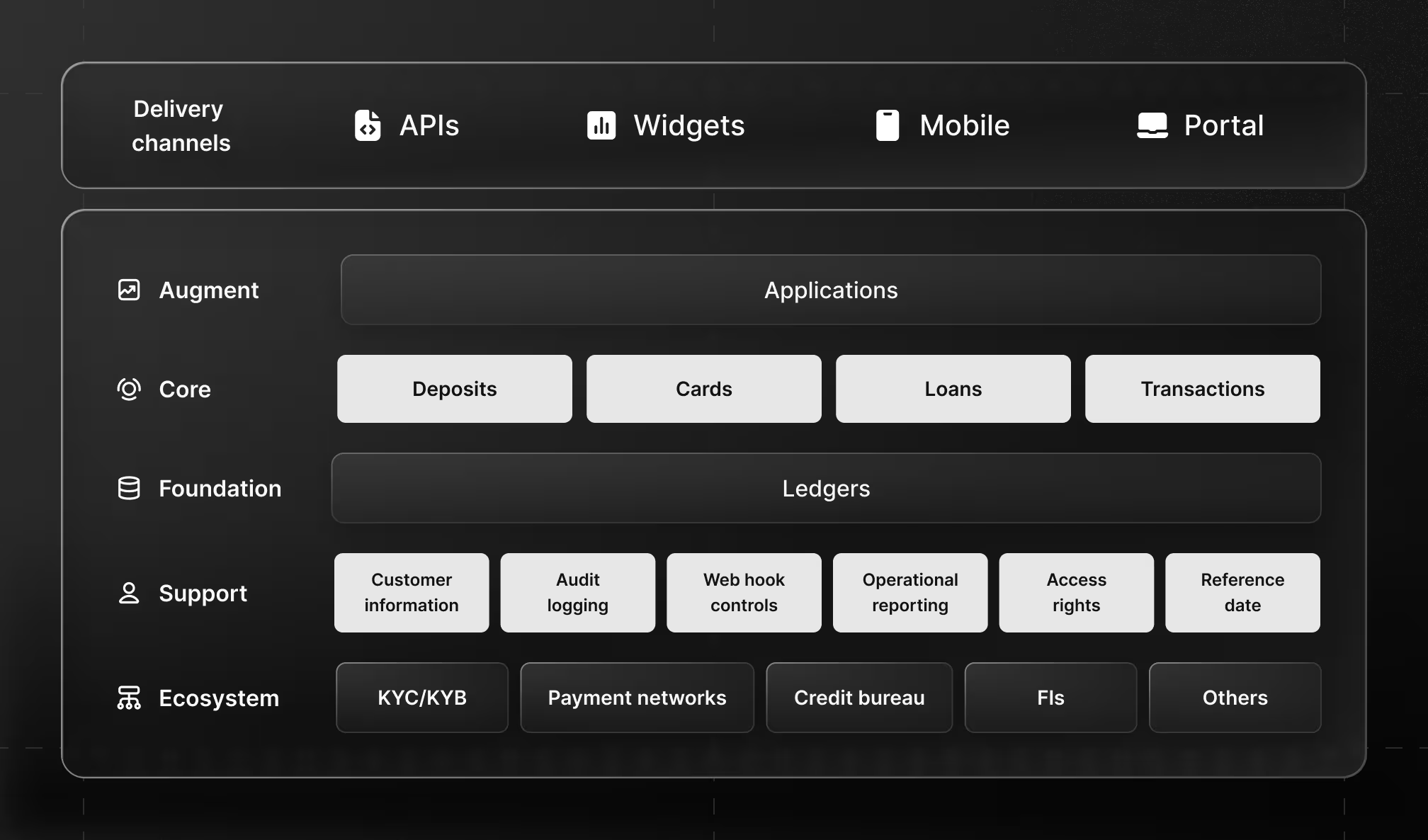

The infrastructure problem

For the consumer, category expansion looks seamless. The experience is clean. The decision is instant. The product feels like one thing.

But from the inside of a financial institution trying to build it: six distinct products, each with different risk profiles, different underwriting logic, different regulatory treatment, and different operational requirements.

BNPL involves small-ticket, high-frequency, soft-credit decisions. RNPL involves large, recurring obligations tied to housing law and tenancy agreements. Healthcare pay-later involves HIPAA, provider billing codes, and repayment volatility linked to life events. Education financing has semester schedules, dropout risk, and long repayment tails. Travel financing has cancellation risk, seasonal exposure, and the complication that the thing being financed hasn't happened yet.

Each of these products requires a different loan decisioning model, different ledger treatment, different disbursement logic, and different regulatory compliance stack. Most financial institutions and fintechs trying to build in this space are attempting to run all of them on infrastructure designed for one: the standard retail instalment product.

That is where things break; in reconciliation mismatches, in credit models that do not account for the right risk factors, in compliance approaches that were designed for consumer retail and do not translate cleanly to healthcare billing or housing law. The failures are invisible to the consumer because the consumer experience is designed to absorb them. The cost lands internally in write-offs, in operational overhead, in the manual processes that quietly patch the gaps between what the infrastructure can do and what the product promises.

The expansion of pay-later is real, and it is structural, and it is not slowing down. But the fundamental question is whether the infrastructure underneath them is built to carry the weight being placed on it or whether it is bending, quietly, under the pressure of categories it was never designed to serve.

Back to the woman booking her holiday. The six-installment travel plan confirmed in three seconds. The rent splitting into her pay cycle as though it was always meant to work that way. None of the seams showing.

Behind that experience, is infrastructure.